Corporate spending in the UAE is going digital; and fast.

Gone are the days of handing out cash, reimbursing employees manually, or using the same shared debit card for every company expense. Today, businesses of all sizes are exploring corporate cards to streamline financial operations, improve spend visibility, and stay compliant.

But here’s the problem: choosing the right corporate card is harder than it looks.

Should you get a credit card, a debit card, or a prepaid solution? What works for your business size? How do you protect against overspending? Can you integrate your cards into your finance stack?

This guide helps you navigate the landscape of corporate cards in the UAE, so you can make an informed choice based on your business stage, structure, and risk tolerance.

The landscape of business payments in 2026

Let’s set the stage.

The UAE is rapidly moving toward cashless business operations. The rise of fintech, new VAT regulations, and increased audit expectations are all pushing companies to abandon petty cash boxes and personal reimbursements in favor of controlled, traceable spending.

But most traditional banks haven’t kept up. They offer complex, outdated card programs with strict eligibility requirements, confusing terms, and limited flexibility.

Startups and SMEs often find themselves stuck between:

- Sharing a single business debit card across the whole team

- Applying (and being rejected) for corporate credit cards

- Tracking expenses manually across Excel, email, and WhatsApp

It’s inefficient. It’s risky. And it’s time to fix it.

There are three main types of corporate cards in the UAE. Let’s explore each in detail.

Option 1: Corporate credit cards (the traditional route)

When most people think of business cards, they think of corporate credit cards ; typically offered by major banks and backed by a credit line.

These cards let you borrow money up to a certain limit, repay it monthly, and often earn perks along the way (such as cashback, air miles, or travel benefits). They’re especially popular with established companies that have stable revenue, long-standing relationships with banks, and mature internal finance processes.

Why businesses choose them:

- Access to working capital via a credit line

- Useful for large purchases or seasonal cash flow gaps

- Offers points and rewards for business travel or procurement

- Enables centralized control for large finance departments

Why they can be problematic:

- Hard to qualify for unless your company has 2–3 years of financial history, audited accounts, and strong revenue

- Often require a personal guarantee from a founder or shareholder ; making you personally liable for debt

- Can carry high interest rates and complex fee structures

- Risk of employee overspending if internal controls are weak

Credit cards can work well for enterprises and larger companies ; but they’re often out of reach (or too risky) for startups, SMEs, and growing teams.

Option 2: Business debit cards (the direct link to your funds)

Next, we have business debit cards ; simple, familiar, and easy to issue once you’ve opened a company bank account.

Unlike credit cards, debit cards draw directly from your company’s available funds. When a payment is made, the money is deducted in real time ; no borrowing involved.

Why businesses choose them:

- Instant access to funds after opening a business account

- No credit check or historical data required

- Zero risk of going into debt or overspending beyond the account balance

Where they fall short:

- Most UAE banks only allow one or two debit cards per account

- You can’t assign a card to every team member or department

- You’re giving employees direct access to your primary business account ; risky if limits aren’t enforced

- Very limited (or no) spend control, merchant blocking, or integration with finance tools

- No audit trail or real-time visibility unless you monitor the account manually

In other words, debit cards are useful for solo founders or very small teams ; but they’re not scalable. Once you have multiple people spending company money, this approach becomes unmanageable quickly.

Option 3: Smart prepaid / Virtual or Physical cards (the modern standard: Pemo)

Now let’s talk about what’s changed ; and why smart prepaid corporate cards are becoming the default for modern businesses.

Prepaid cards work like debit cards ; you load funds onto them, and they can only spend what you’ve allocated. But when combined with finance automation software, they become powerful tools for spend management, control, and visibility.

Platforms like Pemo allow you to issue virtual and physical cards to team members instantly and define exactly how much they can spend, where, and when.

Why smart prepaid cards are becoming the norm:

- No debt risk ; spend is limited to what you load

- Issue unlimited cards for employees, freelancers, or departments

- Set custom spending limits by card, person, or category

- Automatically block certain merchant categories (MCCs)

- Prompt users to upload receipts right after payment

- Fully integrated with accounting tools like Xero or QuickBooks

- Real-time visibility into every dirham spent

You don’t need to qualify for credit. You don’t need to share your bank login. You don’t need to guess who spent what.

Everything is controlled, automated, and traceable ; ideal for startups, SMEs, and scaling teams.

The tradeoff?

- You can’t borrow ; it’s your money, not a bank’s

- You won’t get traditional rewards programs ; though the cost savings from better control often outweigh points

Prepaid corporate cards are especially useful if:

- You’re hiring remote teams or managing contractors

- You want to separate budgets by department or project

- You want to avoid reimbursement chaos and manual accounting

Want to see how it works? Check out our smart corporate cards to explore the features.

Choose Pemo's virtual corporate cards for your team

Pemo offers the best virtual corporate card in the UAE with its expense and team management features, enterprise-grade security, and accounting automation capabilities.

With Pemo, you and your team will get smart virtual cards for your team in the UAE – with $0 set-up fees and 100% visibility into operational spend.

Our prepaid cards sync with MENA #1 spend management software to help you control employee expenses.

Here are some of the standout features of Pemo that our customers love:

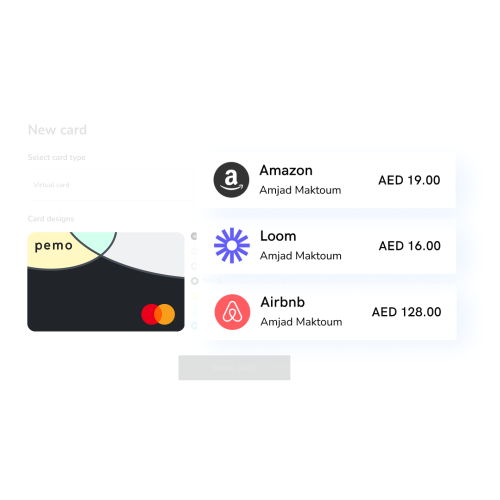

Easily Issue Virtual Corporate Cards In A Click

Pemo enables business leaders to issue virtual corporate cards to their employees with as little effort as a single click.

The features of our virtual corporate cards include:

- Being able to track purchases and view live budgets.

- Real-time visibility that lets you track live transactions on desktop and mobile devices.

- Flexibility for your team by assigning cards to each team member and customize individual spending limits – monthly or per transaction.

- Enterprise-grade security and control, including blocking cards anytime to avoid employee misuse.

- Cashback on online advertising spend (e.g., Google Ads), as well as additional cashback on card spending, such as 2% cashback on FX fees.

➡️ You can create unlimited virtual cards in seconds with Pemo, free of charge.

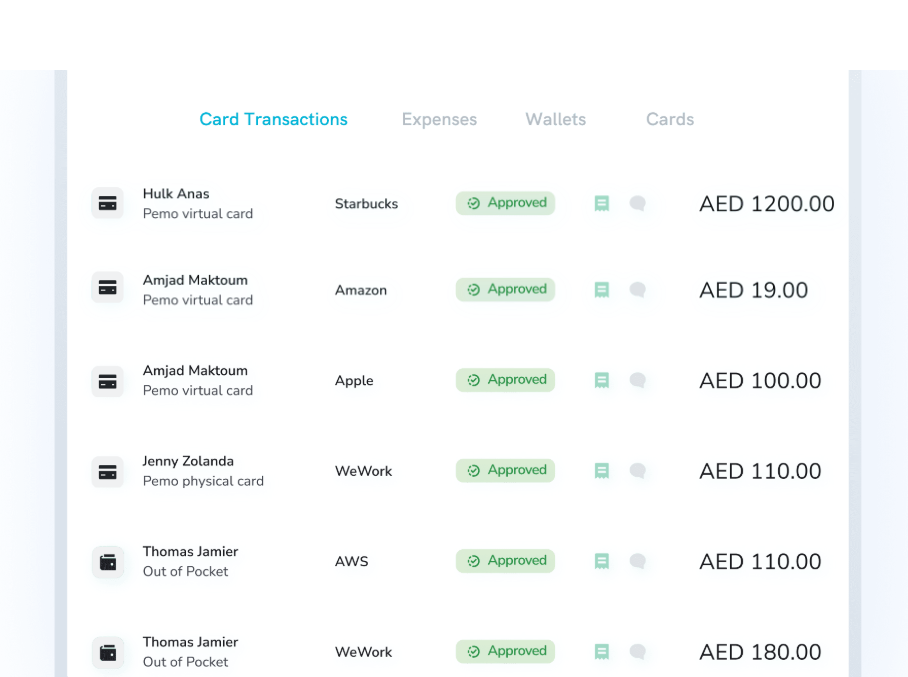

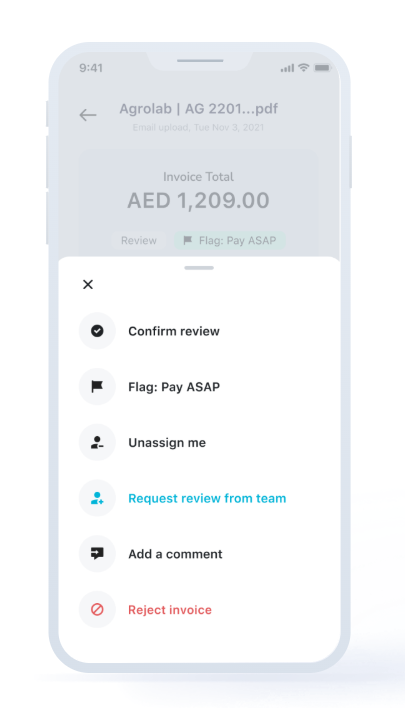

Seamless Expense Management

Pemo helps you eliminate expense reports and petty cash by simplifying and automating your expense reporting.

Our cards and software help you save time doing manual reports by capturing expense data via card transactions and on our mobile app.

You can adjust the spending limit and freeze your employees’ cards live, controlling their spending on the go.

And the best thing about it for your accounting team? Each card transaction instantly turns into a tracked expense.

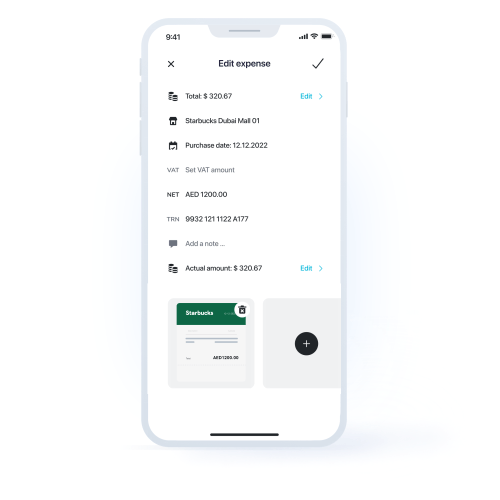

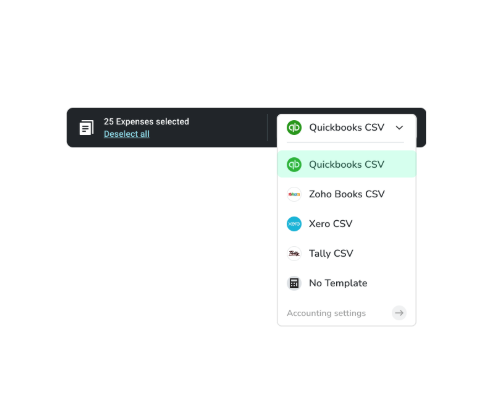

Advanced Accounting Automations

Pemo’s virtual corporate cards will also integrate with your accounting software and ERP, eliminating manual processes for your finance team.

Your employees can seamlessly sync Pemo’s transaction data with QuickBooks, Xero, Tally, and other platforms.

Here are some of the reasons why your accounting department will appreciate Pemo:

- Transaction data flows automatically between Pemo and your organization’s accounting software.

- Your finance and leadership team will get visibility into transactions instantly, syncing them in real-time.

- The expenses are automatically categorized into your chart of accounts.

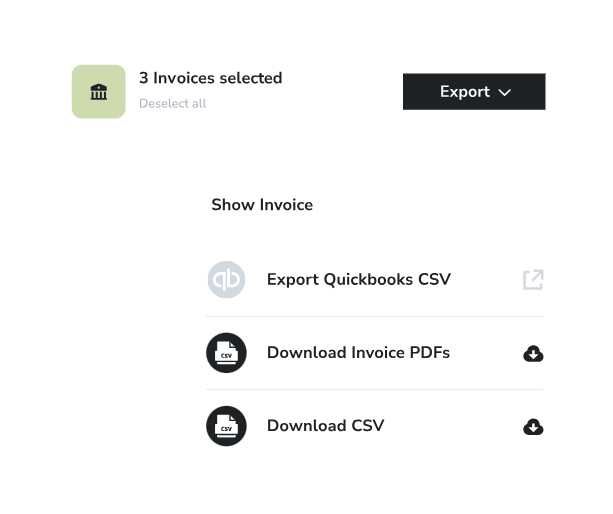

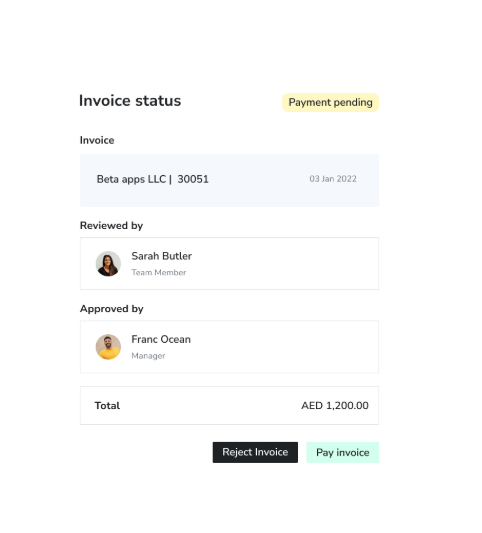

Automate Invoice Payments

Pemo helps you set your invoice payments on autopilot by easily collecting, approving, paying, and managing your bookkeeping for every invoice.

Your team will be able to automate payments, approval flows, and transfers – saving them time.

Approvers will only receive what they need to review and stay in control of upcoming payments.

➡️ Giving your team ownership of their budgets will help them move faster while your finance team is monitoring expenses and signing them off in real-time.

On top of that, Pemo helps you save money from international transfer costs with lower fees than those of some of our competitors.

Pemo’s Pricing

Pemo has a free plan for up to 2 card users that lets you get access to unlimited virtual cards per user with a mobile app, expense reports, card spending limits, and Excel reports of expenses.

To access Pemo’s advanced expense and accounting management features, you’d need to be on one of Pemo’s 2 paid plans:

- Essential: Starts from AED 29/month for 1 card user, which adds cashback on online advertising spend, integration with popular accounting platforms, spend analytics, and more.

- Business+: Custom pricing that starts from 20 card users, which adds additional cashback on card spending, custom onboarding and training, and dedicated CSM.

Want to learn more about Pemo’s Business+ pricing tier to issue virtual cards to your team members, help you eliminate expense hassle, and automate your invoice payments?

You can book a demo with our team and learn more about why 5,000+ companies in the MENA region have chosen us.

Which card is right for your business?

The best corporate card depends on your stage, team size, and financial model.

Let’s break it down with real-world scenarios:

🎯 Early-stage startup (1–10 people)

You’re tracking burn, moving fast, and trying to stay lean. You don’t need credit ; you need control.

Use smart prepaid cards from Pemo to:

- Separate personal and business spend

- Give team members autonomy with guardrails

- Capture receipts and categorize expenses instantly

📈 Scaling SME (10–100 people)

You’re building teams, hiring internationally, and managing budgets across departments. You need visibility and automation.

Use prepaid cards such as Pemo for your teams, integrated with cloud accounting, and consider layering in a credit facility later if your working capital needs grow.

🏢 Large enterprise or corporate (100+ people)

You may benefit from credit lines, procurement cards, and tiered card programs. But even then, control is critical. Many enterprises now combine credit products with spend management platforms like Pemo to stay compliant and efficient.

👤 Sole trader or freelancer

A simple debit card linked to your business account may be enough; but make sure you’re tracking expenses and VAT correctly with cloud tools.

The hidden risks of choosing the wrong card

Still unsure whether your current setup is working? Watch for these red flags:

- You can’t track who spent what without checking your bank manually

- Employees are using their own cards and getting reimbursed later

- Receipts are scattered across WhatsApp, email, and drawers

- You shared your business card PIN or login with a colleague

- You found an old subscription still billing your card for months

All of these are signs that your spend control is broken ; and your current card setup isn’t built for scale.

Next Steps: Sign Up For Pemo For Free

Pemo offers an all-in-one spend management solution for SMBs in the UAE with virtual Visa payment cards that let you to distribute prepaid smart cards to your employees.

Our corporate virtual cards help your accounting team manage expenses through real-time analytics and advanced accounting automations, allowing for better control over finances by setting limits, matching receipts, and tracking expenditures

If you’re looking for a smart virtual corporate card for your UAE-based team that offers advanced features, such as:

- Automated approval flows for invoices.

- Integrations with your accounting software and ERP.

- Real-time cash flow monitoring.

- A comprehensive solution for expense management.

Then you can sign up for Pemo’s free account.