This list runs through the 7 best alternatives to Ramp in 2026: which one fits which use case, and what each costs.

TL;DR

- Pemo is the best Ramp alternative in 2026 for UAE SMEs that want corporate cards, real-time expense tracking, invoice payments, and AI-powered accounting in one platform built for the region.

- If global AP automation matters most, BILL and Tipalti are built around mass vendor payments and international bill pay, while Spendesk and Rydoo lean toward distributed teams that rely on reimbursement and travel workflows.

What are the best alternatives to Ramp in 2026?

The best alternatives to Ramp in 2026 are Pemo and BILL.

Here's my shortlist of the 7 best Ramp alternatives on the market today:

#1: Pemo

Pemo is the best Ramp alternative in 2026 for UAE businesses that want corporate cards, AI-powered accounting, and invoice payments inside one platform built for MENA.

Full disclosure: Pemo is our platform, but I'll give you an honest read on where it stands out and where it doesn't.

We run as an all-in-one spend management platform for SMEs in the UAE and Saudi Arabia. Cards (Visa and Mastercard) are issued in minutes.

Expense tracking happens in real-time. AI accounting categorizes everything before your bookkeeper opens the file.

Here's where Pemo holds up specifically against Ramp. 👇

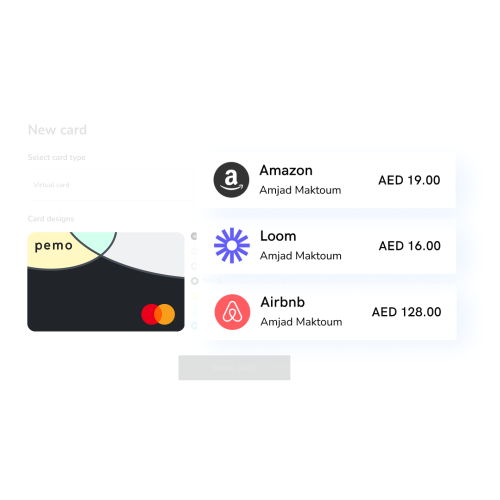

AED-native corporate virtual cards

Pemo’s cards work in AED, plug into the regional accounting stack your finance team already uses, and handle VAT the way the FTA expects.

A few things our customers tell us they value about how this works:

- Visa and Mastercard from one platform, so you're never blocked by a merchant or government portal that only takes one network.

- Unlimited virtual cards in seconds, which means your marketing lead can roll a card for Google Ads without filing a finance ticket.

- Single-use cards that close themselves after the first transaction, useful when a vendor's payment terms shouldn't turn into an unexpected recurring charge.

- Pre-spend rules that decline a transaction at the moment of swipe if it falls outside policy. The trigger could be the spend amount, the type of merchant, the specific vendor, or the time of day.

Cards can be frozen in two taps from the app, and physical cards arrive at your office within 72 hours of approval.

Receipt capture that runs in the background

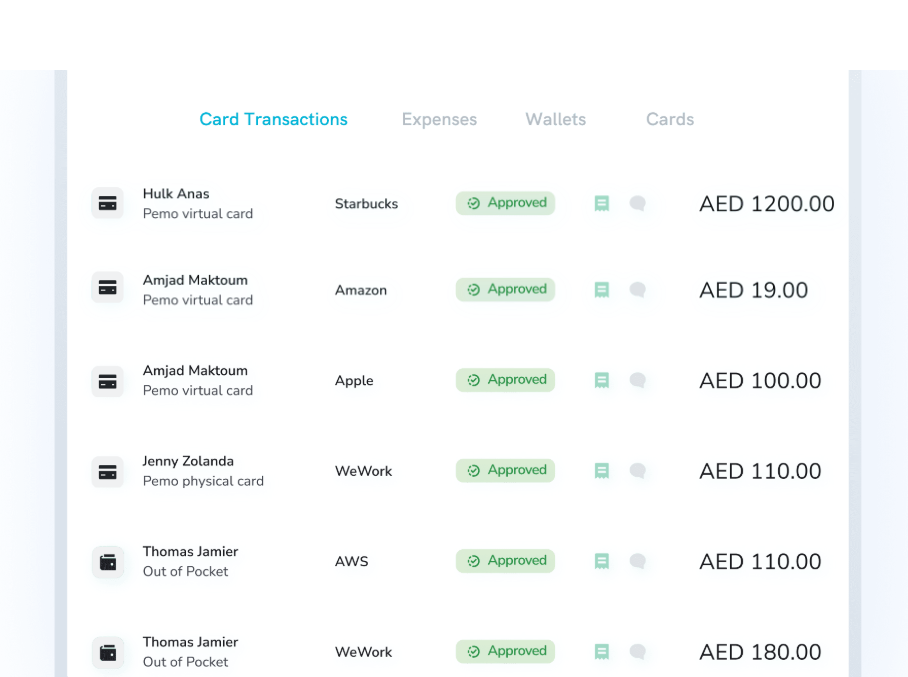

Pemo’s entire workflow is shaped around how UAE finance teams actually close their books.

Every card transaction lands in the Pemo dashboard the second the swipe clears.

Your team member gets a push notification asking for the receipt, our AI matches the photo to the right transaction, and the expense moves into whichever approval flow you've set up.

Approval chains run on whatever logic your team already uses. Big-ticket purchases need a second approver.

Department heads sign off on their own line items. Travel cost categories route through whoever owns the office.

You configure it once, and the rules enforce themselves.

Out-of-pocket reimbursements follow the same flow, so card spending and personal card spending live within one process instead of two.

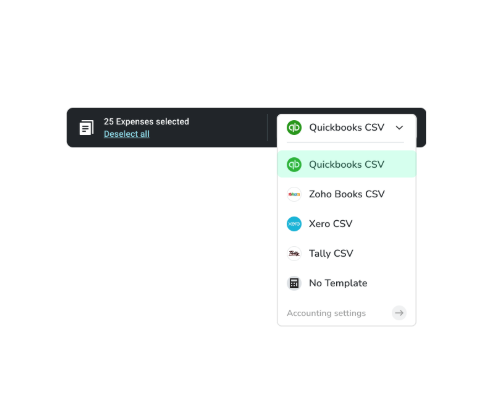

Books that close themselves with Pemo Copilot

Pemo Copilot is the AI layer doing the bookkeeping work in the background.

Every transaction gets sorted into the right Chart of Accounts category, paired with the correct vendor, and tagged for VAT treatment - using the patterns it picks up from how your bookkeeper has handled similar entries in the past.

The longer your team runs spend through the platform, the sharper its predictions get.

Direct integrations push the categorized data into:

- QuickBooks and Xero, the cloud accounting tools most common among UAE SMEs.

- Zoho Books and Wafeq, the regional favorites that most UAE-focused tools support natively.

- Tally and Microsoft Dynamics 365, for businesses running ERP-grade accounting setups.

- Custom CSV exports, in case your accounting stack isn't on the supported list.

Pemo's Pricing

Pemo's free Kickoff plan covers up to 2 card users. Unlimited virtual cards, basic expense management, invoice capture and payment, AI receipt matching, and accounting integrations all sit on the free tier.

For more depth, there are 2 paid plans:

- Essential: AED 29/month per cardholder. Adds team organization, custom approval workflows, multiple wallets, and expanded analytics. A 10-person team comes out around AED 290/month.

- Business+: Custom pricing for teams of 20+ cardholders. Adds advanced analytics, enhanced cashback rates, a dedicated account manager, and priority support.

Want to learn more? You can sign up for Pemo's free plan or book a demo to see it in action.

Pemo's Pros and Cons

✅ Real-time expense tracking on one dashboard.

✅ A good range of accounting integrations, including Wafeq and Zoho Books for the regional stack.

✅ Visa and Mastercard, issued together.

✅ AI accounting that gets sharper with use.

✅ Free plan for two cardholders.

❌ Cards are prepaid, and weekend wallet top-ups can be tricky since bank transfers don't clear outside business hours.

#2: BILL

Best for: Finance teams that want a free corporate card and budgeting tool, with the option to bolt on paid AP and AR modules.

Similar to: Tipalti, Spendesk.

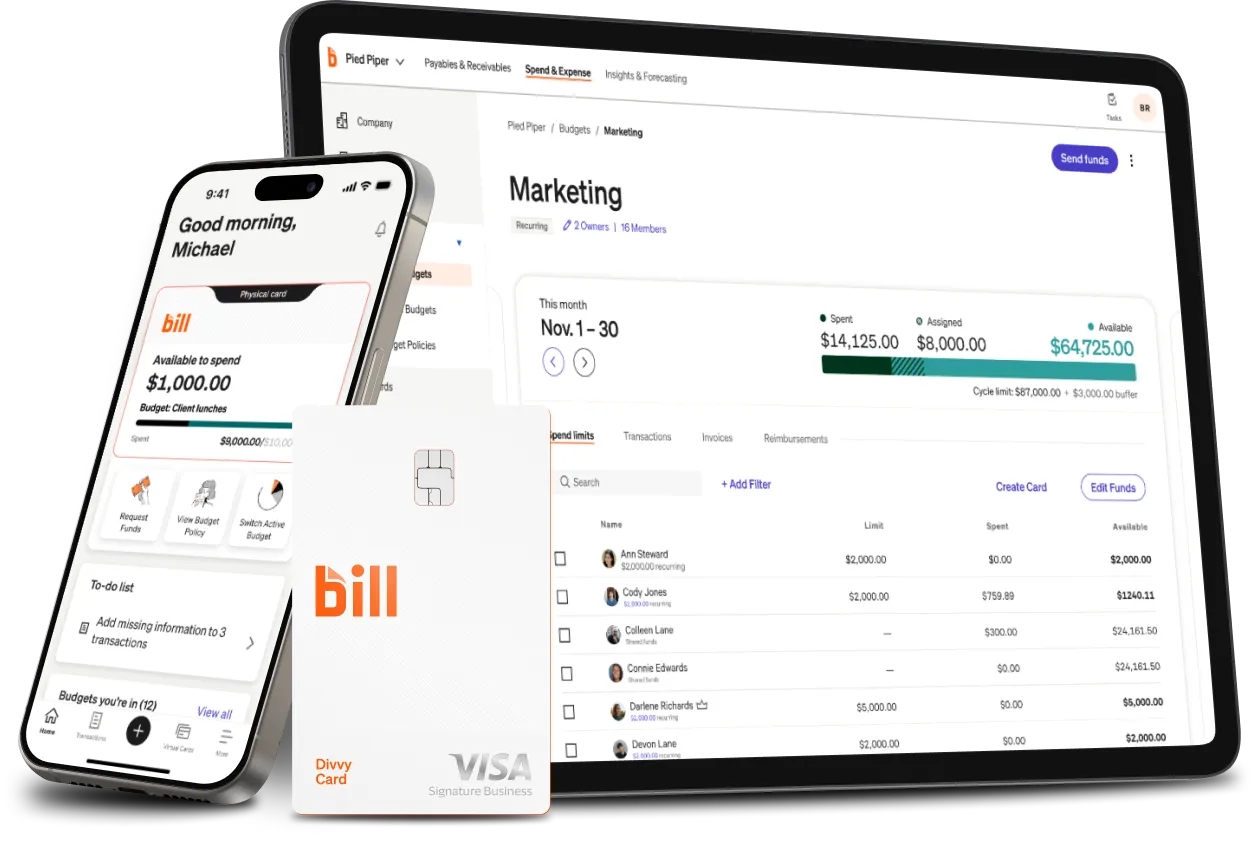

BILL runs two products that together overlap with most of what Ramp does: BILL Spend & Expense (formerly Divvy), which handles corporate cards and budgets at no per-user cost, and BILL AP & AR, which handles vendor bills and customer invoicing on a paid plan.

For UAE-based teams that want both sides, this combination puts card spend, vendor bills, and customer payments under one login.

Features

- The BILL Divvy Card with credit lines that range from $1,000 to $5 million depending on business profile.

- Budget pools and live spend tracking built into the free Spend & Expense tier, with no per-user charge.

- AP and AR in one workflow, with approval policies that route by vendor, role, or amount threshold.

- Two-way accounting sync with QuickBooks, Xero, NetSuite, and Sage Intacct on the paid AP and AR plans.

Pricing

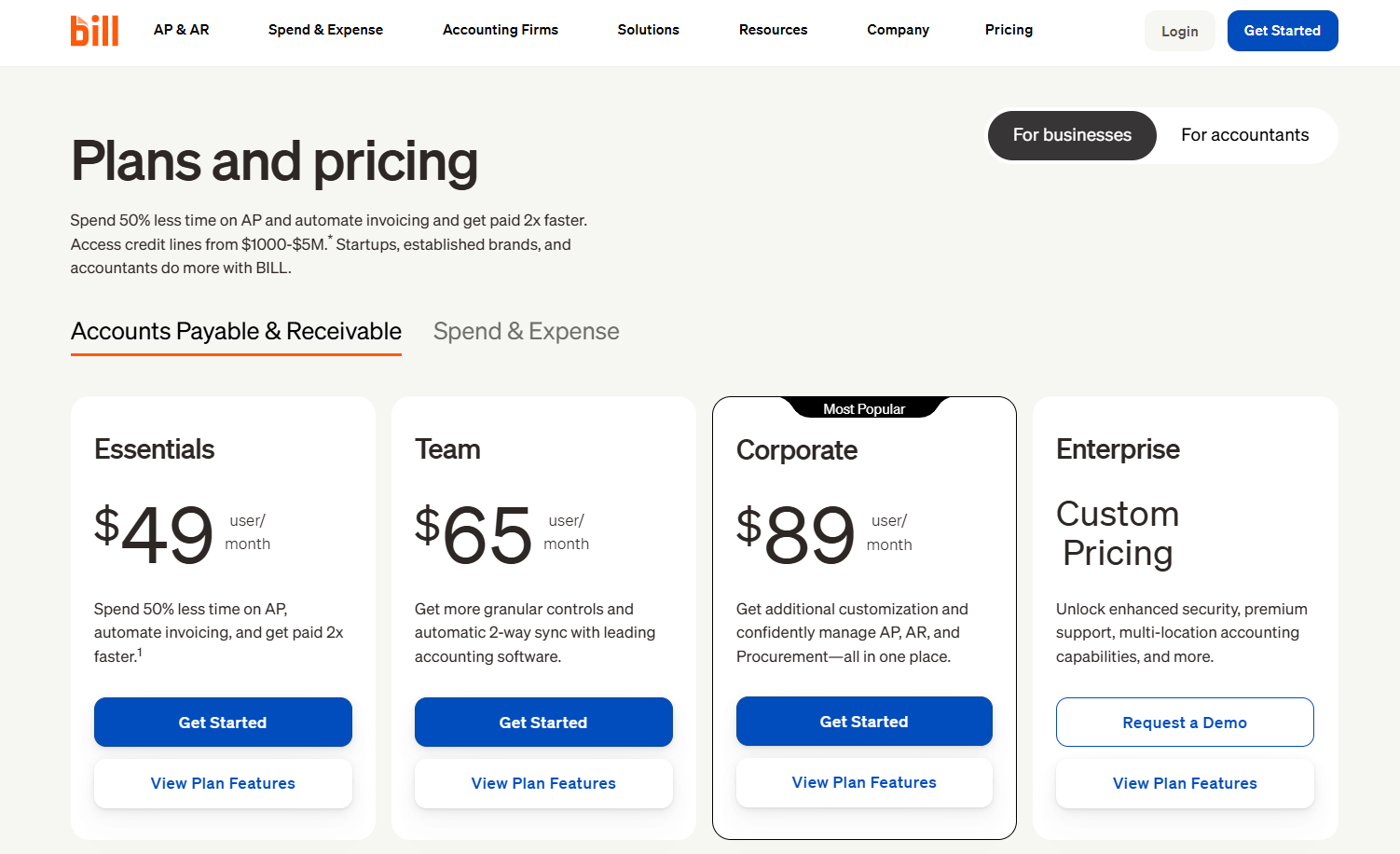

BILL has four pricing tiers:

- Essentials: $49/user/month. Includes basic AP and AR functionality with live chat and phone support.

- Team: $65/user/month. Adds automatic 2-way accounting sync and custom user roles.

- Corporate: $89/user/month. Adds combined AP and AR management with custom approval policies.

- Enterprise: Custom pricing. Adds premium support, multi-location accounting, and extra integrations.

Pros and Cons

✅ Spend & Expense product is genuinely free.

✅ Strong native sync with NetSuite, QuickBooks, and Xero.

✅ Credit lines available for qualifying businesses.

❌ One user mentions that they find it challenging at times to map and integrate custom fields or make changes to existing fields.

#3: Spendesk

Best for: Distributed finance teams that want reimbursement, invoice management, and card spend in one workflow.

Similar to: BILL, Pleo.

Spendesk pulls spending approvals, employee reimbursement, and invoice handling into a single workflow, with reach across the UAE and Europe.

The fit is best for teams that lean heavily on out-of-pocket spending and need the reimbursement loop to feel as clean as the card workflow.

Features

- Mobile reimbursement submission where employees photograph receipts and the right approval chain handles the rest.

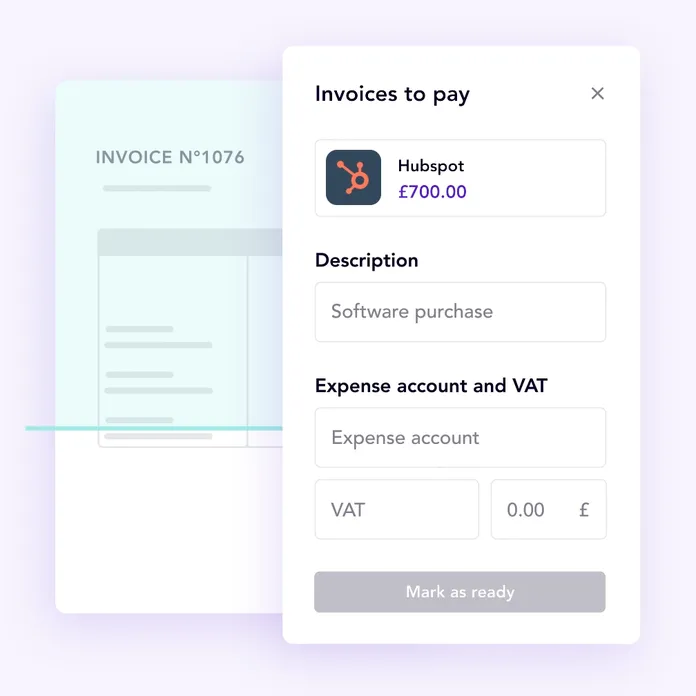

- OCR-based invoice capture with duplicate detection that catches suspicious bills before they get paid twice.

- Live expense visibility that surfaces missing receipts and policy breaks before reporting deadlines roll around.

- Budget controls applied across teams, with spend caps enforced as transactions happen.

Pricing

Spendesk uses custom pricing, so you'd need to contact their team for a quote tailored to your team size and feature needs.

Pros and Cons

✅ End-to-end invoice management with accounting integrations.

✅ Catches duplicate invoices and data entry mistakes automatically.

✅ Real-time budgeting controls.

❌ Pricing is not transparent.

#4: Tipalti

Best for: Finance teams running global accounts payable and mass vendor payments at scale.

Similar to: BILL, Spendesk.

Tipalti is the global AP engine of this list, with payment infrastructure designed for businesses paying vendors across multiple currencies and tax regions.

If the most painful part of finance for your team is moving money internationally, this is the closest match for Ramp's AP work.

Features

- Cross-border payouts spanning 196 countries and over 120 currencies, with rails covering SWIFT, ACH, local transfers, and more.

- Card reconciliation that handles Mastercard, Visa, AmEx, and Tipalti's own card on the same dashboard.

- Auto-sync to NetSuite, Sage Intacct, and QuickBooks, which takes manual data entry out of the monthly close.

- Self-service supplier portal where vendors update banking and tax info on their own, instead of finance running an email thread.

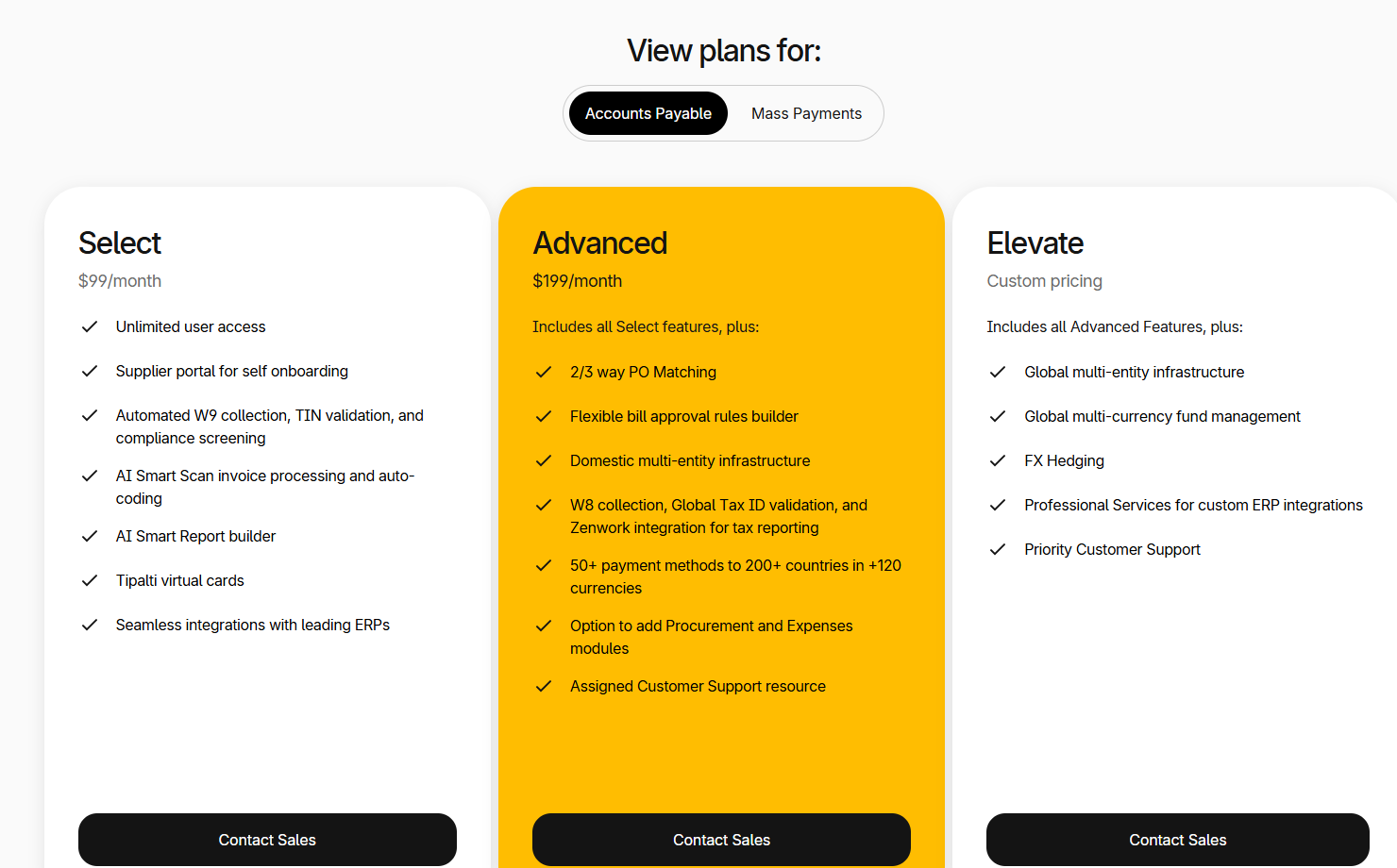

Pricing

Tipalti has three pricing tiers:

- Select: $99/month. Covers the supplier portal, AI-powered Smart Scan invoice capture, the bill approval rules builder, and ERP integrations.

- Advanced: $199/month. Adds procurement features, multi-entity multi-currency setup, mass payments as an add-on, and 2-way and 3-way PO matching.

- Elevate: Custom pricing. Includes the full procurement solution, budget management, and Slack integrations.

Pros and Cons

✅ Built for genuine global AP. ✅ Vendor self-service portal cuts back on email tag.

✅ Native NetSuite sync.

❌ Higher starting price at $99/month than some of the other competitors on the market.

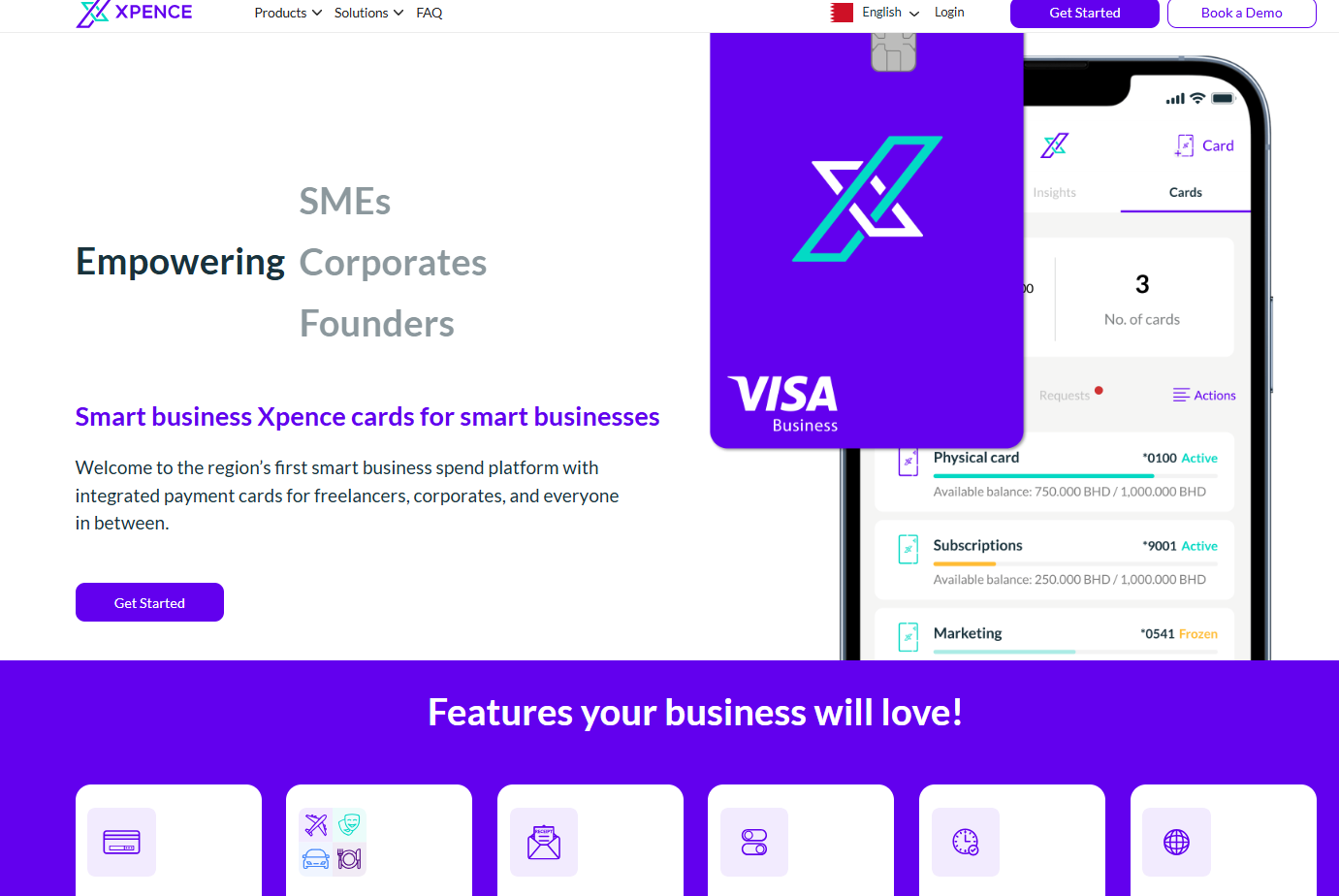

#5: Xpence

Best for: UAE teams that want virtual Visa cards with SaaS subscription tracking and live spend controls.

Similar to: Pemo.

Xpence's angle is straightforward: virtual Visa cards plus SaaS subscription tracking, all running off real-time transaction categorization.

It's a closer fit for finance teams whose biggest budget question is software subscriptions and online tools, rather than where physical cards are getting swiped in stores.

Features

- Auto-categorization in real-time as each transaction lands in the dashboard.

- SaaS subscription tracking with renewal alerts and per-tool cost analytics.

- Spending controls layered per card, user, and category, so each cardholder operates inside their own guardrails.

- Centralized visibility across cards, vendor payments, and software subscriptions in one view.

Pricing

Xpence doesn't share its pricing publicly. You'd need to contact their team for a walkthrough and a custom quote.

Pros and Cons

✅ Built for SaaS-heavy spend stacks.

✅ Approval workflows included.

✅ Detailed spend controls.

❌ No public pricing, unlike many Xpence alternatives.

#6: Mamo

Best for: UAE merchants that want corporate cards and merchant payment acceptance under one login.

Similar to: Pemo.

Most spend platforms keep two things separate: paying out to vendors and taking payments from customers. Mamo doesn't.

It's a regional payments platform that puts both sides into the same dashboard, useful for SMEs that both pay vendors and take customer payments through cards, payment links, or e-commerce checkouts.

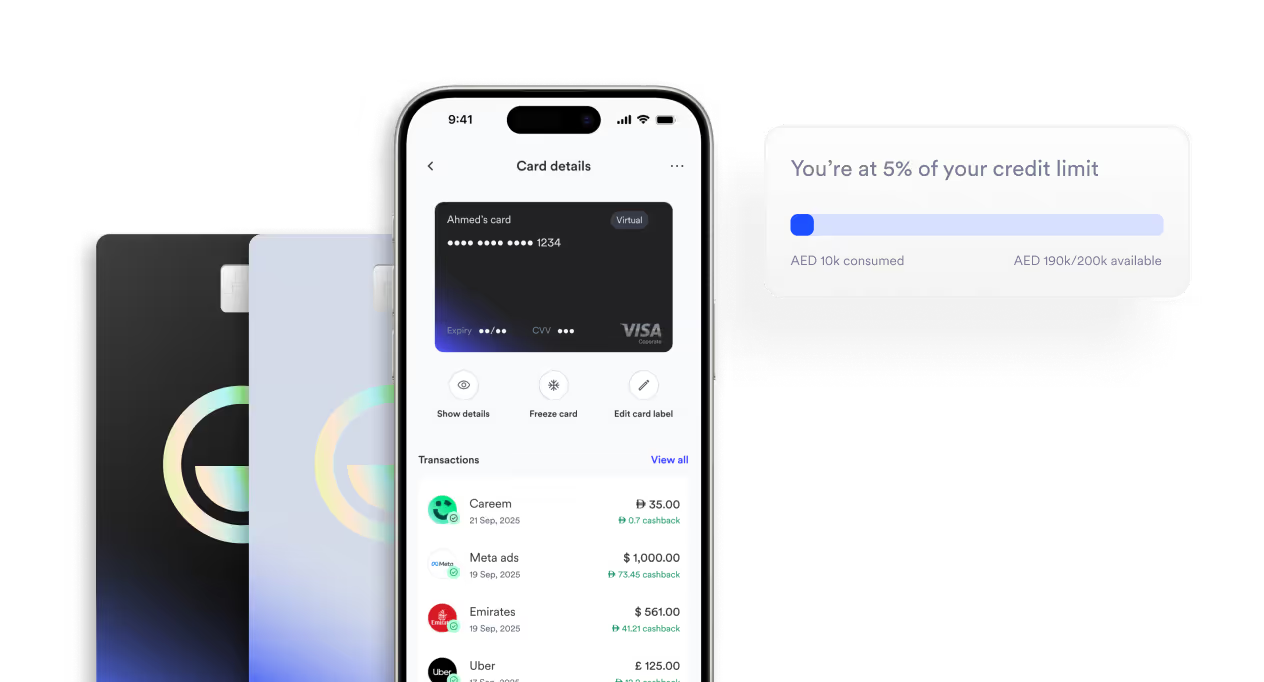

Features

- Two sides of one platform: corporate cards your team uses to pay vendors, plus payment links and APIs your finance team uses to take customer payments.

- Cashback on global card spend, capped at 2% for transactions in currencies other than AED.

- No issuance ceiling on cards for both virtual and physical formats.

- PCI-DSS-grade fraud monitoring with live transaction visibility and one-tap card freeze if something looks off.

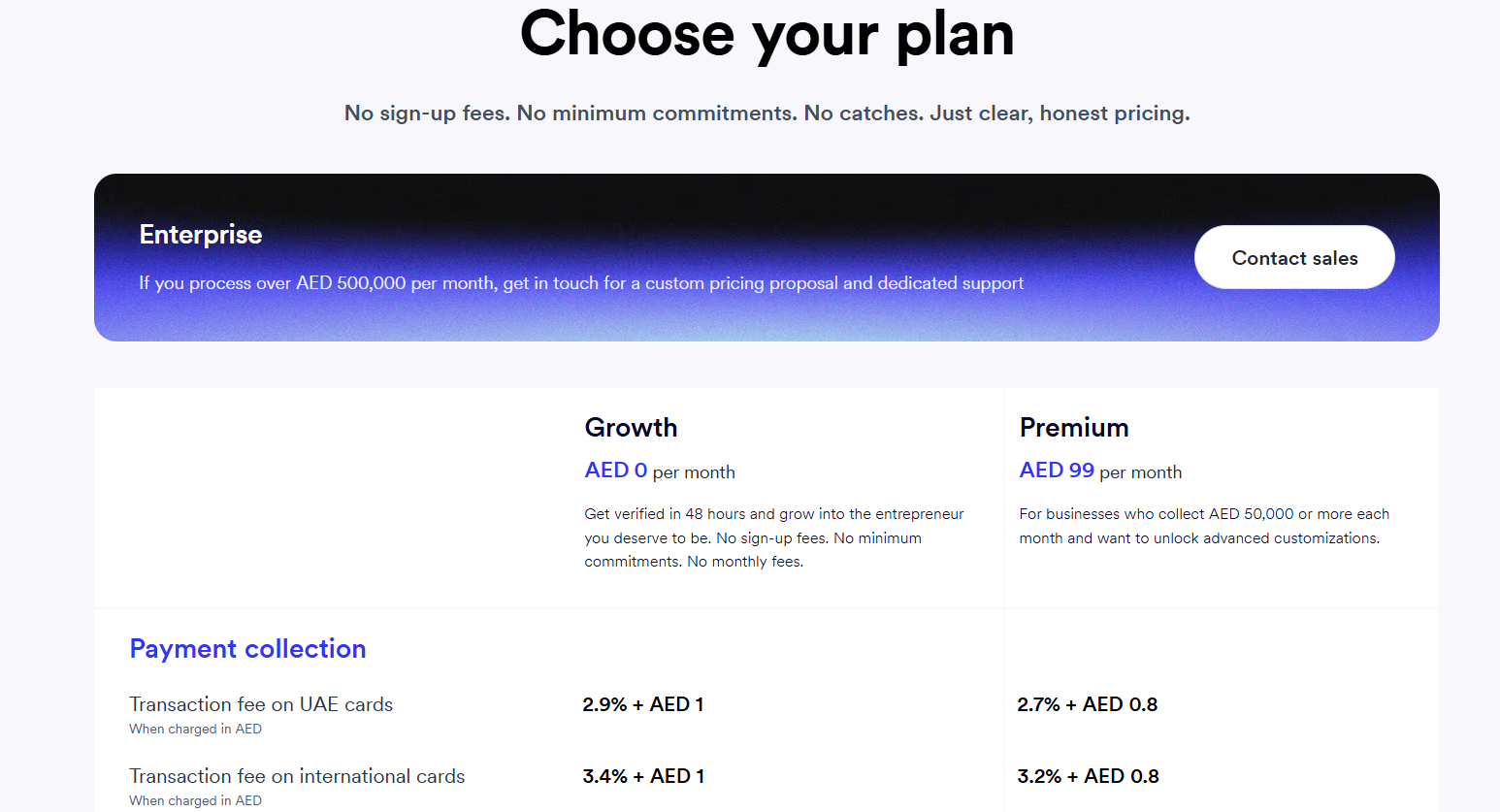

Pricing

Mamo offers three tiers:

- Growth: Free monthly fee, with 2.9% + AED 1 per accepted payment. Includes corporate cards and payment APIs.

- Premium: AED 99/month, with transaction fees dropping to 2.7% + AED 0.8. Adds free UAE ATM withdrawals and branded payment links.

- Enterprise: Custom pricing for businesses processing more than AED 500,000/month, with a dedicated CSM included.

Pros and Cons

✅ Combines payment acceptance and corporate card spend.

✅ Cashback on non-AED transactions.

✅ PCI-DSS certified.

❌ 2.9% plus AED 1 per transaction on the free plan can add up with heavy usage.

#7: Rydoo

Best for: Finance teams handling expenses, travel, and per diem allowances at scale.

Similar to: Spendesk, Tipalti.

Rydoo is the AI-driven expense platform on this list with the strongest emphasis on travel and per diem workflows.

The right pick when employee expenses, trip-based costs, and policy enforcement carry more weight than the corporate card and AP automation that Ramp leads with.

Features

- Smart Audit AI trained on policy and expense compliance, flagging non-compliant or suspicious claims as employees submit them.

- Ten-second receipt scans with 95%+ accuracy on auto-populated expense fields, pulled from a single photo of the receipt.

- Policy logic that adapts by country and role, so a Dubai team's per diem rules don't have to match a London team's.

- Finance dashboards that update live, instead of refreshing on a daily or weekly schedule.

Pricing

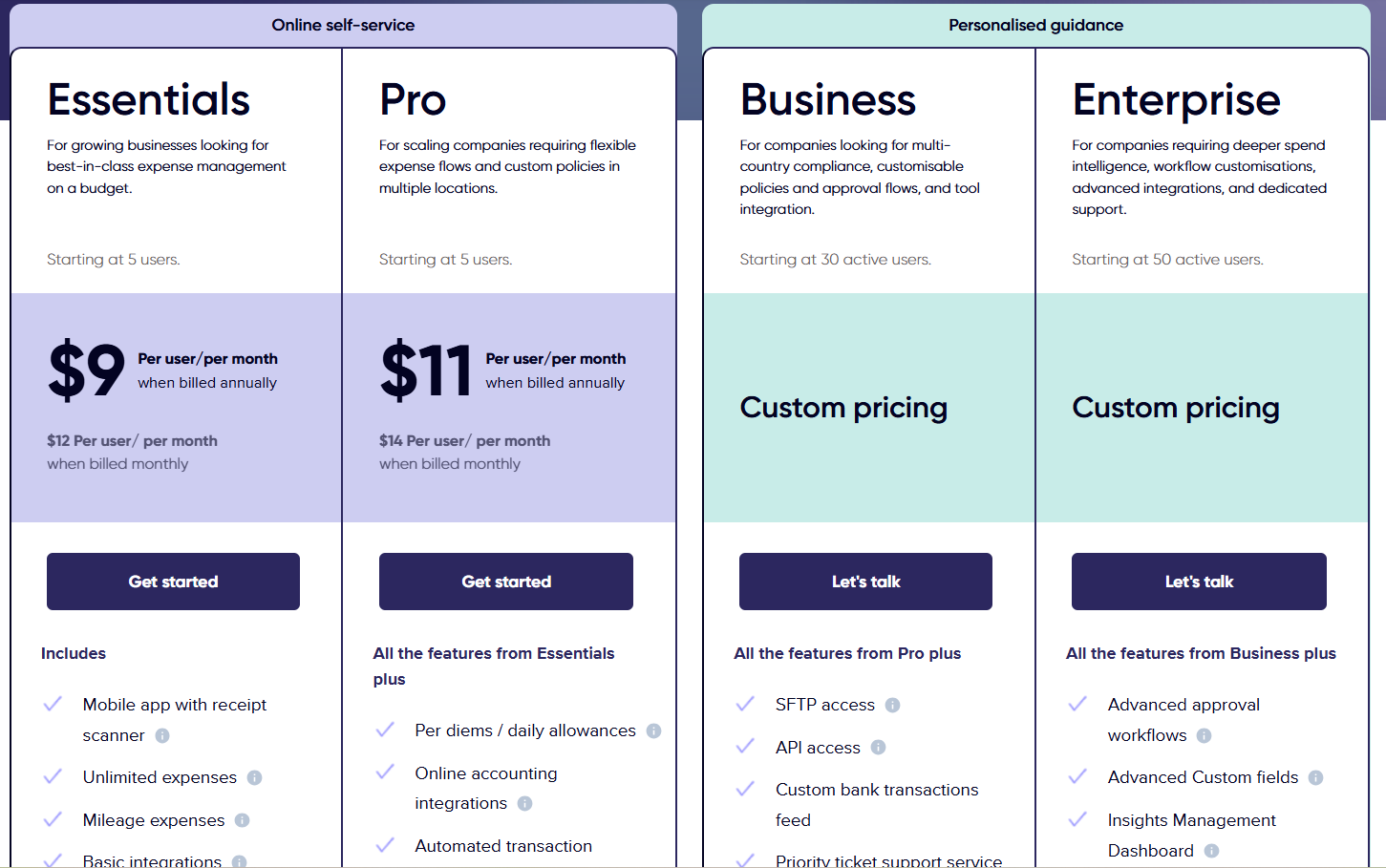

Rydoo has four pricing tiers:

- Essentials: $9/user/month annually. Includes the mobile receipt scanner, unlimited expense submissions, and basic integrations.

- Pro: $11/user/month annually. Adds per diems, online accounting integrations, and customizable policies.

- Business: Custom pricing. Includes SFTP and API access, custom bank feeds, and priority support.

- Enterprise: Custom pricing. Adds advanced approval workflows, SAML SSO, and an insights dashboard.

Pros and Cons

✅ Easy front-end for employees submitting expenses.

✅ Receipt scanning saves time on field expenses.

✅ Strong fit for travel-heavy teams.

❌ Business and Enterprise plans do not have public pricing.

Try Pemo for free

If you’re looking for:

- AED-native Visa and Mastercard cards from one platform, no FX gymnastics required.

- No US bank account or $25K minimum to qualify.

- Native integrations with Wafeq, Tally, Zoho Books, and the rest of the regional accounting stack.

- AI categorization that learns your Chart of Accounts logic over time.

Then you can sign up for the free Kickoff plan, or book a demo with our team if you want to walk through how Pemo handles your specific accounting setup.

⚠️ Disclaimer: This article was last updated on 8th of May, 2026, and if there's any misinterpretation of the information, please contact us, and we will fact-check it.